News |

Reports

Equity Capital Markets Update, November 2025

U.S. Market Commentary

Key U.S. Macro Themes

Administration, Trade, and Economic Growth

- The longest government shutdown in U.S. history ended November 12th after a measure was passed to fund operations through January 2026

- U.S. – China trade agreement took effect this month, with China rolling back various export restrictions on rare earth materials to the U.S.

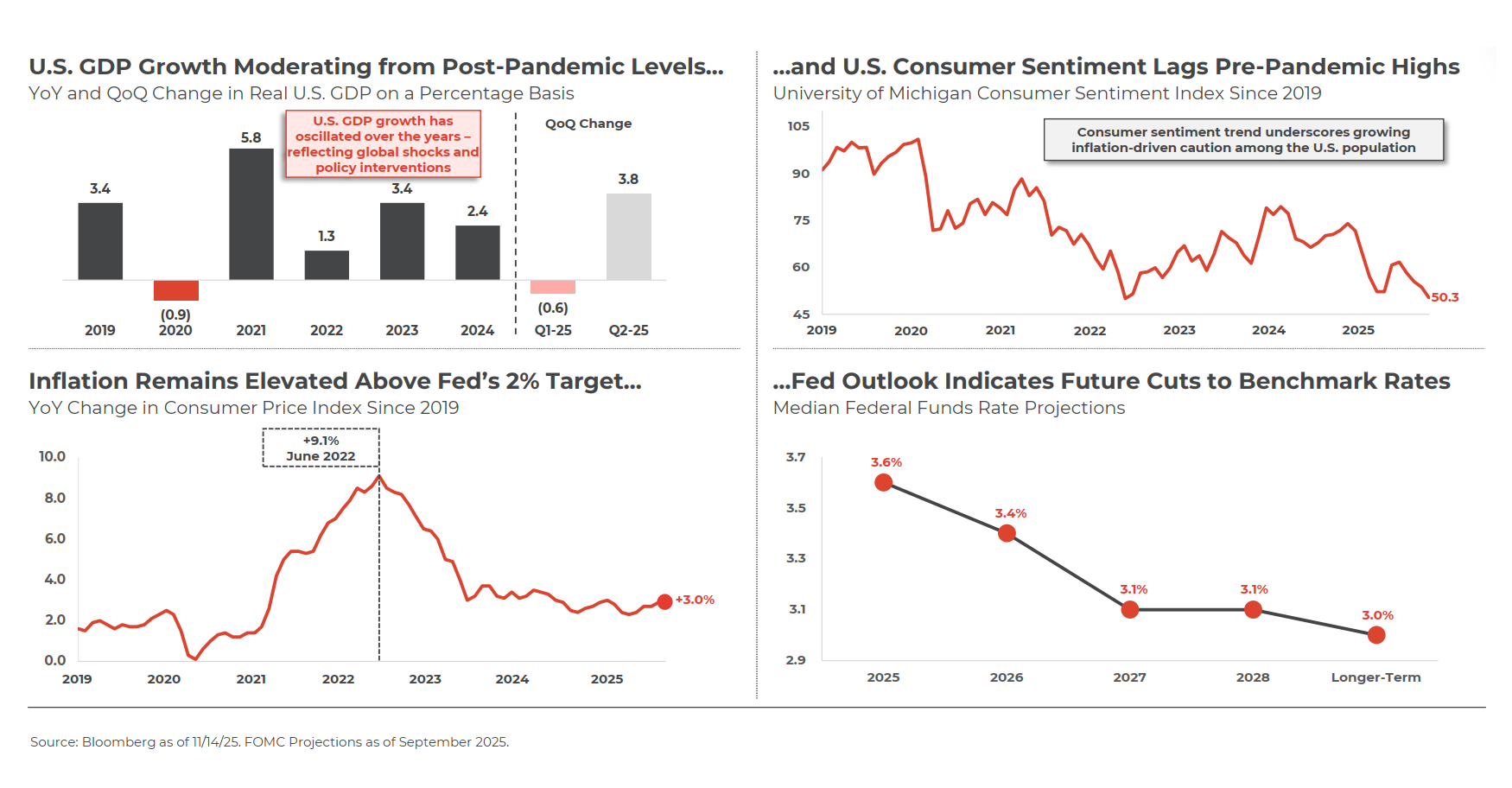

- U.S. real GDP growth forecasted to land in the 1.4 – 1.7% range, with the latest official projections expected to be released following the December FOMC meeting

Monetary Policy, Labor Market, and Inflation

- Federal Reserve implemented a 25bp cut to benchmark rate at October meeting, bringing target FFR range to 3.75% – 4.00%, and stated a halt to balance sheet run-off starting December 1st

- Recent commentary from Fed officials lowered the market’s expectations for additional 25bp cut in 2025 – currently ~42% vs. ~96% probability before the October FOMC meeting

- Private sector employment data from ADP indicates U.S. companies shed ~11k jobs per week for the 4-week period ended October 25th

- U.S. CPI rose 3.0% for the 12-month period ended September 2025 – the only official economic data that was released during the shutdown

- U.S. Administration officials stated critical October economic data (i.e., jobs and inflation figures) are unlikely to be released

Source: Bloomberg, FactSet, FOMC, ADP. Market data as of 11/14/25. Issuance figures exclude SPAC IPOs

U.S. Equities Overview

Public Equity Markets

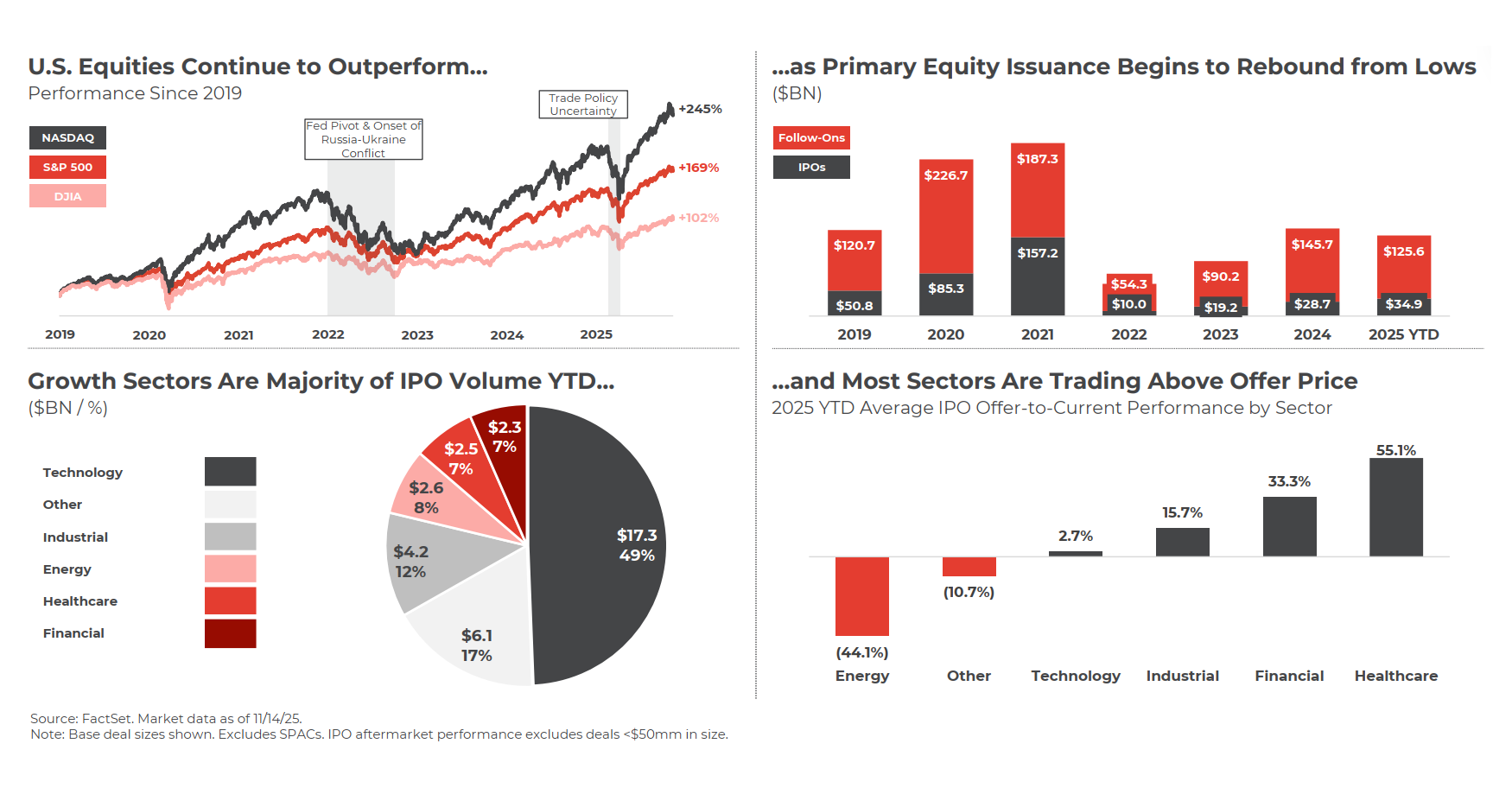

- S&P 500, Dow, and NASDAQ performance was modestly positive for the four-week period ended November 14th

– Finished the period up +1.1%, +2.1%, and +1.0%, respectively

– YTD performance is up +14.5%, +10.8%, and +18.6%, respectively

Equity Capital Markets

- Over the last four weeks, 15 IPOs representing ~$3BN and 58 follow-ons representing ~$12BN have priced across a variety of sectors

- Notable transactions include:

– BillionToOne – $314mm IPO – +50.0% offer-to-current

– Evommune – $173mm IPO – +14.4% offer-to-current

– Exzeo Group – $168mm IPO – (14.7%) offer-to-current

– BETA Technologies – $1,167mm IPO – (7.7%) offer-to-current

– Navan – $923mm IPO – (32.7%) offer-to-current

– MapLight Therapeutics – $288mm IPO – (17.1%) offer-to-current

Source: Bloomberg, FactSet, FOMC, ADP. Market data as of 11/14/25. Issuance figures exclude SPAC IPOs

Contact ARC Group Securities

Please fill in the contact form and we will reach out to you as soon as possible.