Year in Review, 2025

U.S. Macro & Policy Backdrop

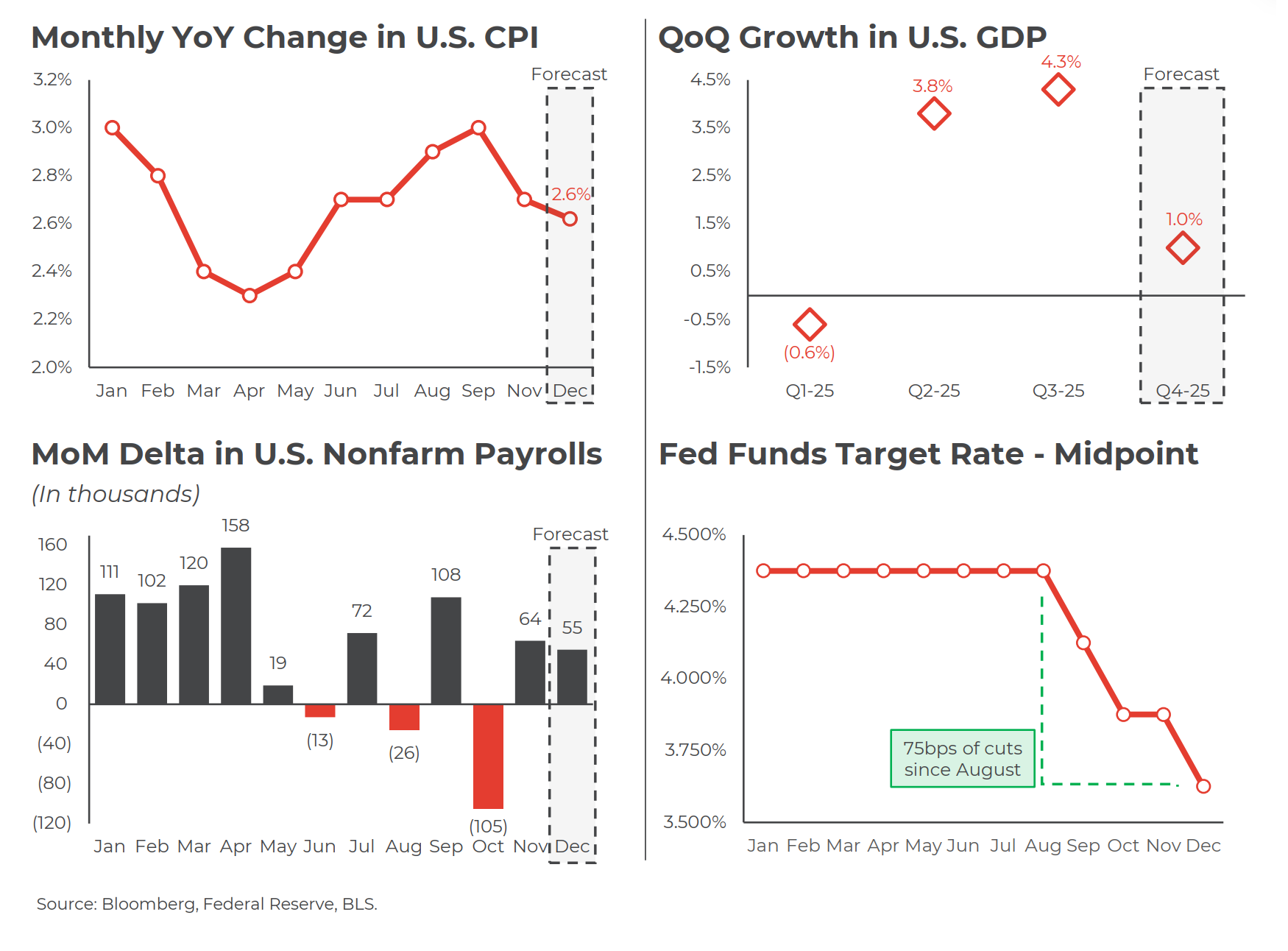

2025 Recap: Economic Momentum Endures Despite Political Noise

In 2025, the U.S. economy demonstrated surprising resilience, defying widespread recession expectations as growth ticked higher despite restrictive monetary policy and elevated geopolitical uncertainty. Inflation unevenly decelerated from the highs, which enabled the Federal Reserve to pivot from peak benchmark rates, while maintaining a cautious stance. In terms of policy, U.S. tariff uncertainty weighed on business and consumer confidence as companies delayed or recalibrated their strategies amidst the unpredictable backdrop. The U.S. labor market gradually rebalanced, marked by slower job growth and easing wage pressures, but remained historically tight at ~4.3% unemployment.

Outlook for 2026: Sturdy Growth and Selective Potential Headwinds

Outlook for 2026: Sturdy Growth and Selective Potential Headwinds

The U.S. economy expects to remain on a path of moderate, trend-like growth, supported by resilient consumer spending, easing financial conditions, and continued capex investments into the broader AI buildout. Markets expect inflation to drift slightly lower towards the 2% target and a relatively stable employment environment, signaling a soft-landing scenario. Key implications as we move into 2026 include an AI rollover, a new Fed Chair, and faster-than-expected acceleration of the economy due to fading trade war shock driving higher inflation.

U.S. Equities Markets

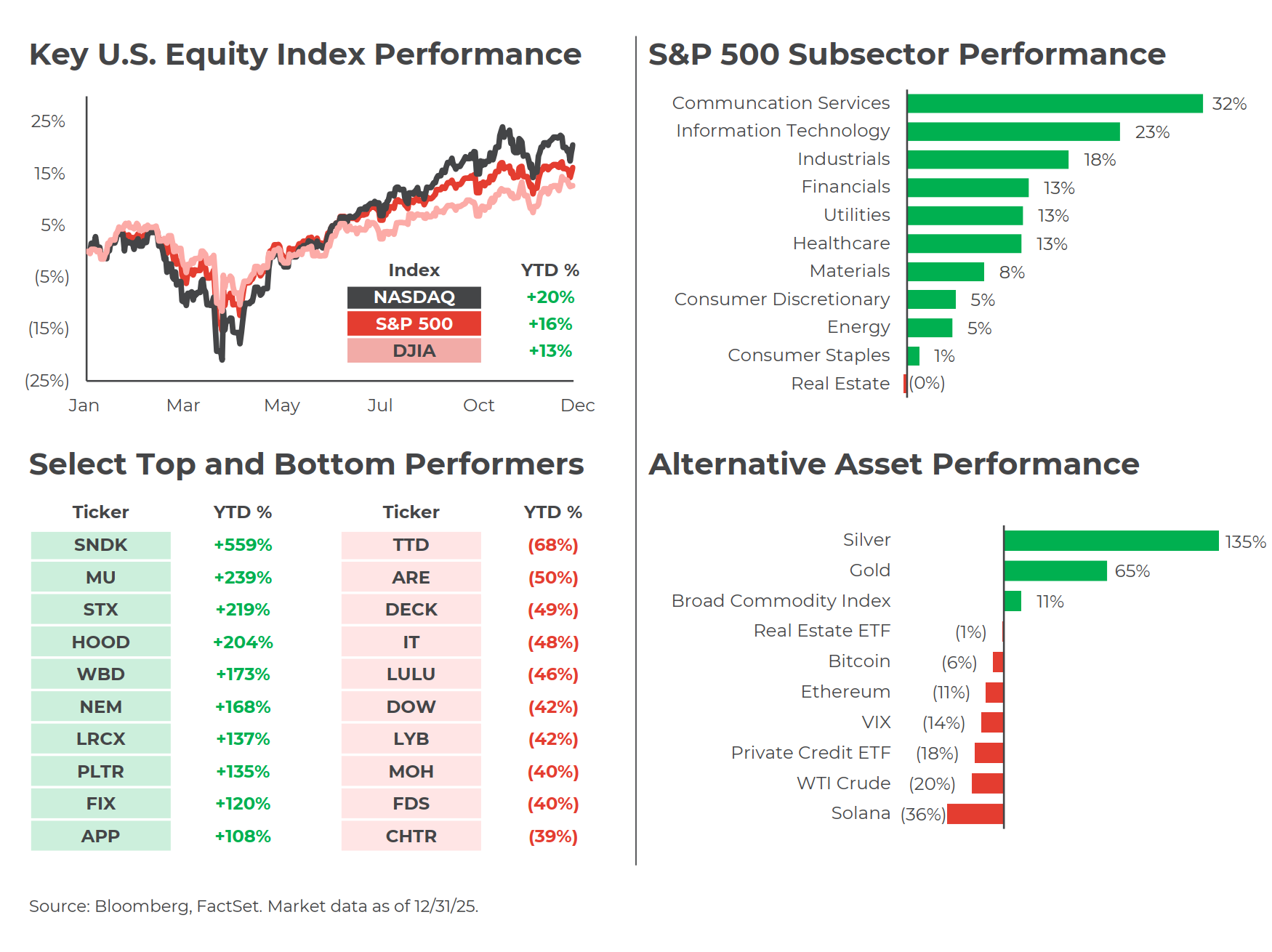

2025 Recap: The Bull Market Charged Forward

U.S. equity markets posted strong gains in 2025, underpinned by a durable economic backdrop, improving inflation dynamics, and a view that monetary policy reached peak restrictiveness. The market put up its third year of consecutive double-digit gains – the third instance since the GFC. Large-cap and technology oriented subsectors drove performance across indices, where earnings growth and the pervasive AI capex and digital infrastructure trades supported elevated valuations. Speculative and high-beta names also saw outsized gains, reflecting easing financial conditions, renewed retail participation, and investor willingness to reprice longer-duration growth assets due to lower forward rate expectations.

Outlook for 2026: Core Drivers Point to Continued Strength

Outlook for 2026: Core Drivers Point to Continued Strength

Looking ahead to 2026, the outlook for U.S. equities looks constructively balanced, supported by expectations for moderate economic growth, and profit growth is poised to continue – S&P 500 earnings expected to grow 14% in 2026. As the AI cycle is largely financed by profitable, cash-rich firms and underpinned by robust global demand, investors expect the outperformance to continue into the new year; although volatility is expected as the market struggles to price a technology that is advancing at exponential speed. Geopolitics, U.S. midterms, and new Fed leadership to remain top of mind for investors.

U.S. Equity Capital Markets

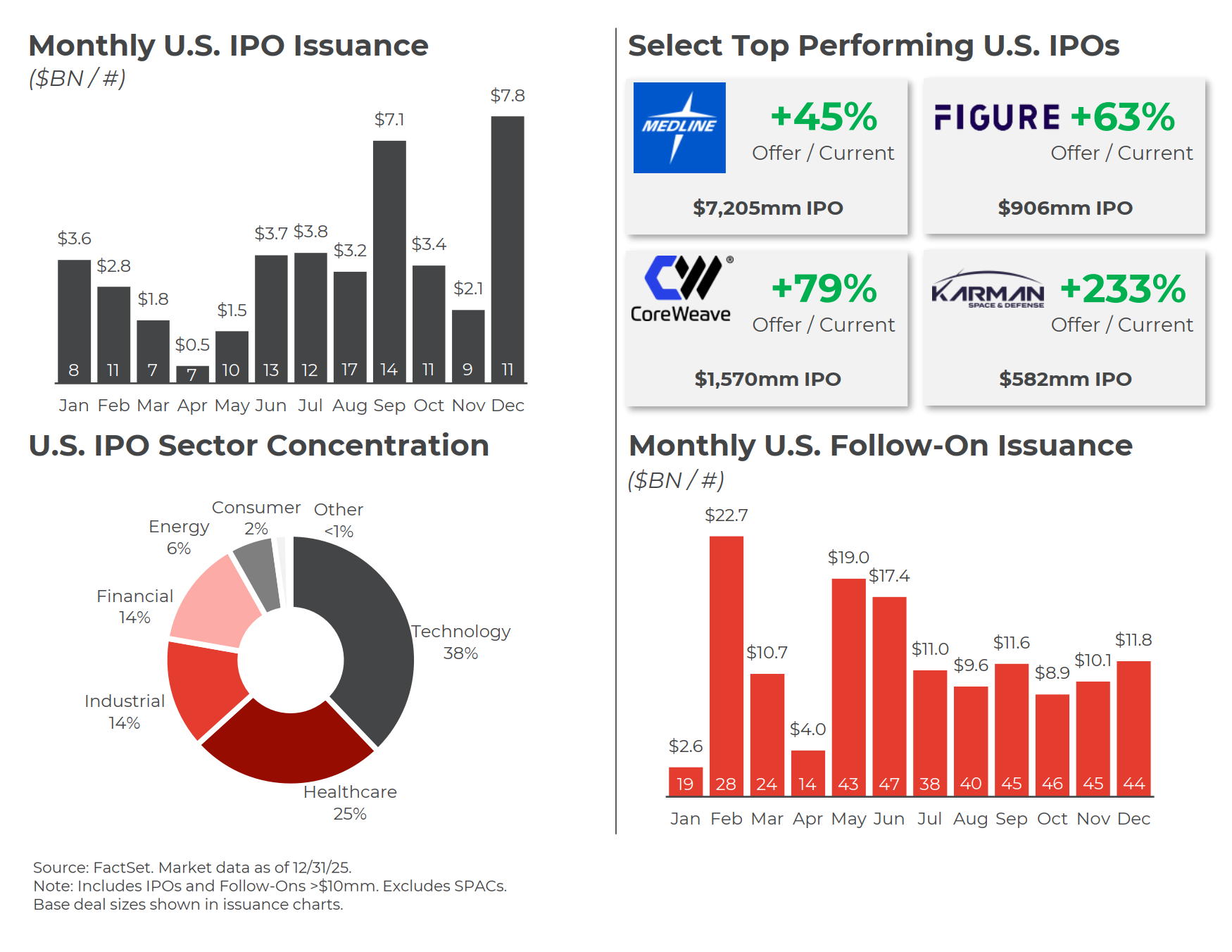

2025 Recap: Year of the IPO Resurgence

Following a post-COVID cooling-off period, the initial public offering window creaked back open, led by multiple high-profile and AI-driven companies, leading the most active year for IPOs since 2021. The comeback did not occur in a straight line – tariff volatility caused several major players to put their offerings on hold until the market found its footing. Away from Technology, we saw a sizable quantum of primary issuance from names in the Healthcare and Industrials sectors, which provided confidence inspiring proof points that the window was open to a broader range of themes than AI-driven technology. Additionally, PE sponsors renewed their willingness to utilize the public markets as an exit path this year.

Outlook for 2026: Extension of Equity Capital Markets Momentum

The IPO pipeline expanded significantly, with multiple scaled, high-profile companies preparing to tap the public markets in 2026. The street expects the current backlog and improved market receptivity to IPOs with clear paths to profitability and differentiated business models to be key drivers for issuance in the coming year. While pockets of private capital are the deepest they have ever been in history and companies are staying private for longer – Databricks, for example, raised a $4BN Series L at a $134BN valuation – investors are ultimately looking to the public markets to monetize these stakes.

U.S. SPAC Market

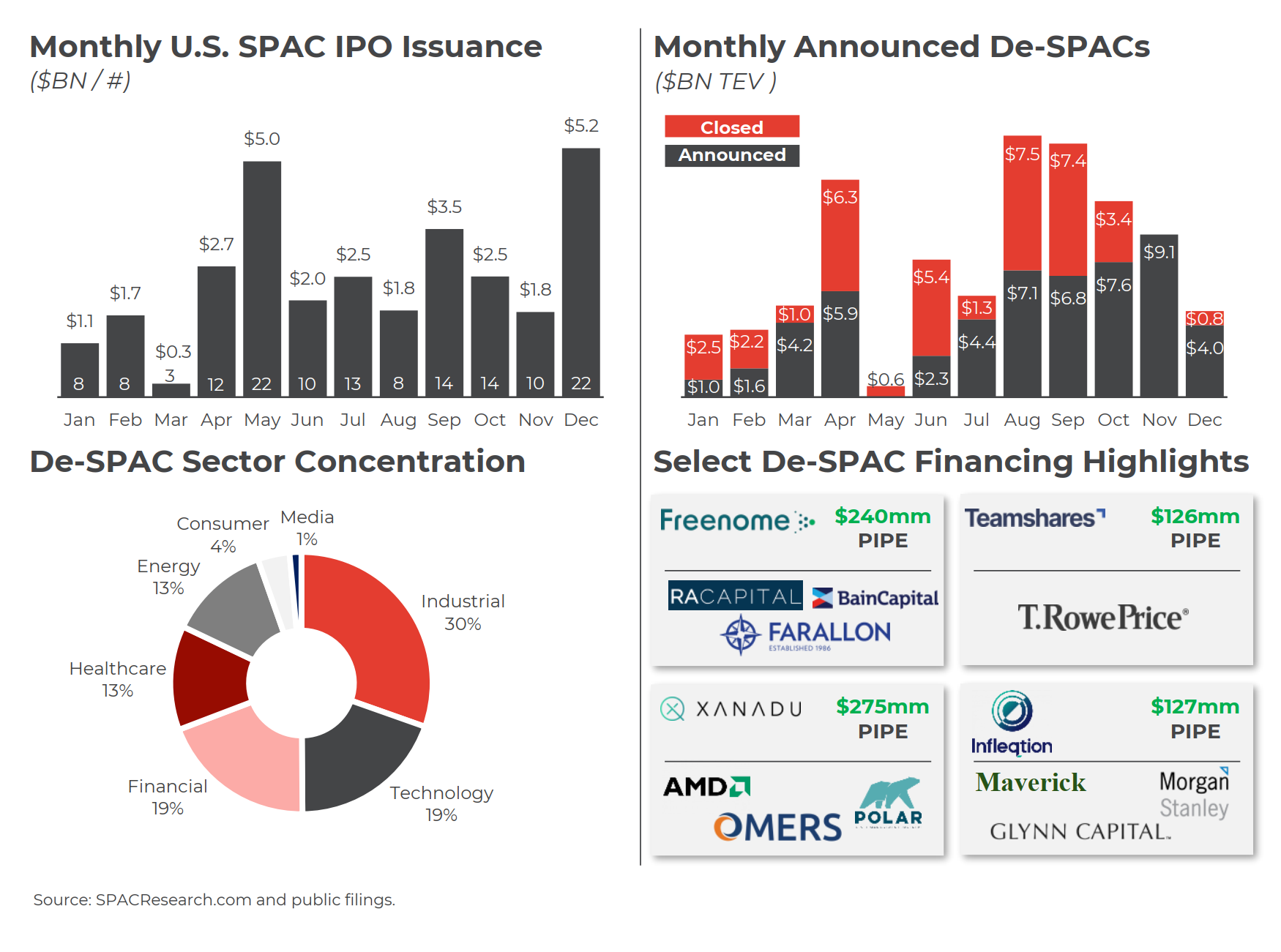

2025 Recap: Robust Issuance Supported by Broader Equity Backdrop

Similar to the regular-way IPO market, the SPAC market showed a meaningful rebound from the subdued issuance levels over the prior years across both SPAC IPOs and De-SPACs. In terms of front-end issuance, we saw $30BN of SPAC IPOs this year – more than the previous three years combined and over two times the level of volume in 2019. Announced De-SPAC activity in terms of enterprise value totaled ~$54BN, which is in-line / at the higher end of prior years excluding 2020 and 2021. There was ~$38BN of closed volume this year, down from both 2023 and 2024 – key point of focus as the SPAC IPO market continues to fire on all cylinders.

Outlook for 2026: Test of the Full SPAC Lifecycle

Moving into 2026, it will be a pivotal year of execution for the vintage of SPACs that have priced in 2025 to structure deals, announce them to the market, and rotate their shareholder bases. Provided the broader macroeconomic, policy, and equity market backdrops remain conducive, we should see a pickup in announced De-SPACs and capital recycled back into SPAC IPO issuance. As deal performance improves, the market can expect to see investors continue to dip their toes back into the PIPE market and further solidify SPACs as a viable route to the public markets for emerging, high-growth companies.

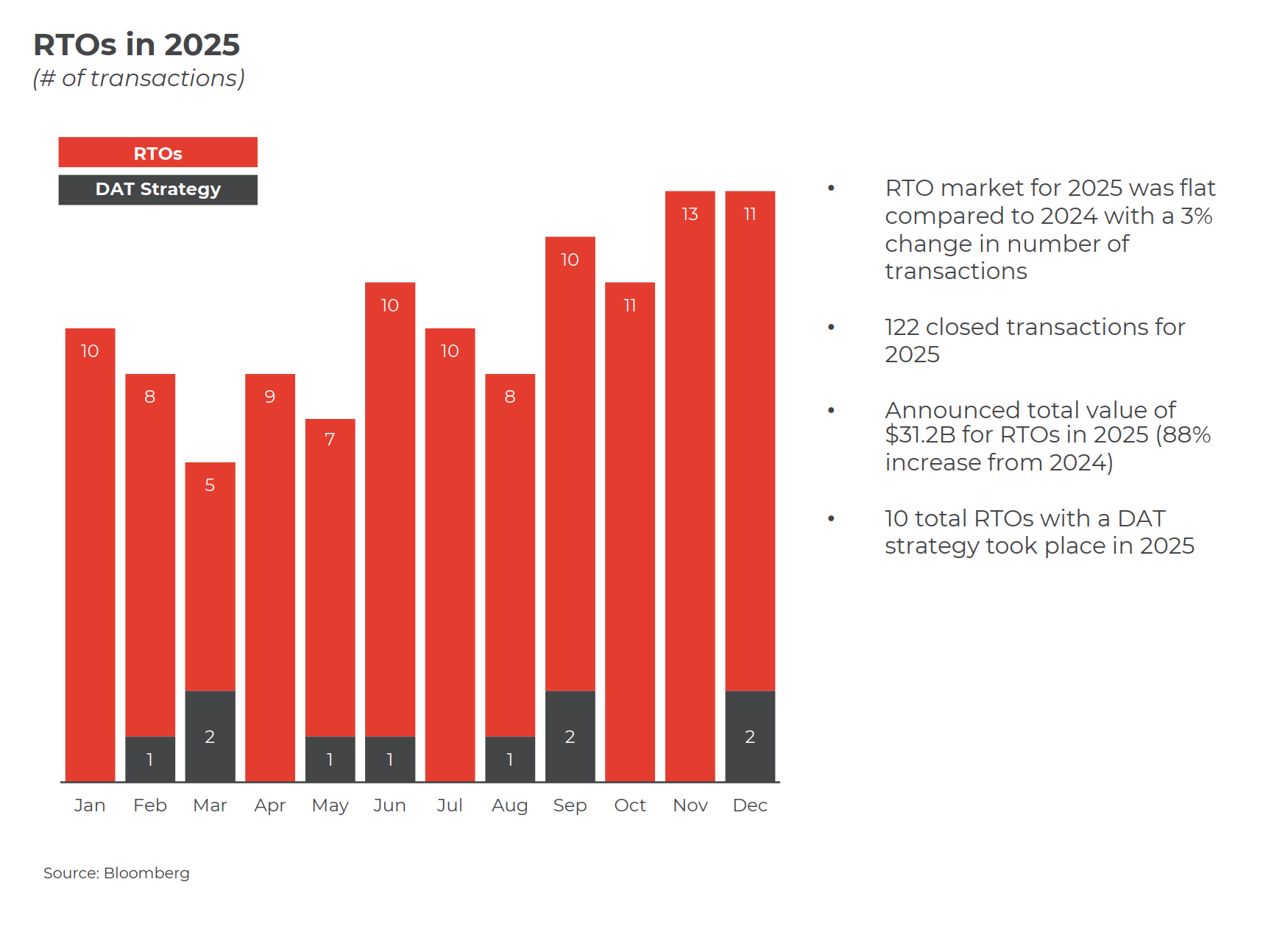

Alternative Listings and RTOs

2025 Recap: DAT Hype Surged and Deflated, Shrinking RTO Activity

2025 was a particularly active year for Reverse Take Overs or RTOs with many of the most famous transactions being Digital Asset Treasuries (DAT). The first DATs would raise money to re-invest directly into crypto currencies kept in a treasury account. These initial deals had great institutional investment participation in the first half of the year. After the initial excitement, successful DAT deals with institutional participation quickly fell off. What was left were many shell companies and listings with inflated prices based on the DAT wave. This limited the number of traditional RTOs we saw through the year as a transaction via RTO did not have the same cost efficiency we have seen in past years.

Outlook for 2026: Shell Activity and Stricter Compliance Boosts RTOs

We have seen pricing of shells already trend towards market rates of early 2025 with the fall off of DAT deals. We also expect that there will be additional shells on the market based on the more rigorous continued listing requirements coming from the exchanges such as NASDAQ. These factors should combine to make RTOs a cost-efficient listing method and as a result could be a good year for RTO transactions. Increased diligence will be a key point of focus to ensure listing compliance going forward.

Key 2026 Predictions

Contact ARC Group Securities

Please fill in the contact form and we will reach out to you as soon as possible.